It’s really difficult for me to believe that this is my first review of Biorem. Have had many requests to look at them and with each quarter those requests grow. I can no longer ignore the will of the people. Perhaps I should deny more requests for shitco’s, but dumping on and exposing bad companies brings me too much joy.

Only so much time in the day - but the day for Biorem has arrived.

Is this chart sexy enough for you? From .95 at the start of the year up to $2.21 at closing yesterday. Market reaction to these results a couple of days ago has been a little muted. Great ride. Does it have more room? Let’s review.

Balance Sheet:

If you haven’t noticed, when I look at a company’s current ratio I like to remove deferred or unearned revenue from current liabilities. I understand why it’s accounted for that way and other accounting guru’s might frown on my methodology. If you disagree, go write your own fucking review - this is my house.

Biorem’s current ratio is a very good looking 2.9 that consists of $3.9M in cash, $10M in receivables. $2M worth of inventory and $5M of other short term assets against $7.2M of liabilities due over the next twelve months.

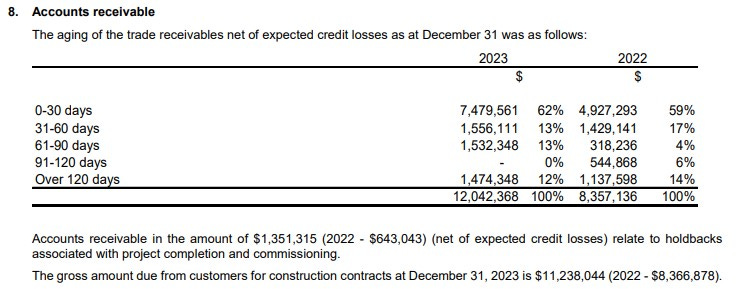

If you are a frequent reader of mine, then you know I like as much disclosure as possible in the notes of the financial statements. Biorem falls short here with their quarterly financial statements consisting of only eleven pages and ten notations. 50% of their current assets are tied up in receivables while their cash accounts for less than 19%. When a company’s A/R is this substantial, I want to see an aging report and Biorem does not provide one. I have to go back to their annual statements to get one and that raises some concerns with 38% over 30 days and a more concerning 25% over 60 with 12% over 120 days. When you don’t disclose things like this, I immediately assume you’re trying to hide something. That’s my nature. I know you know what the aging looks like as of June 30th, so share it with your investors.

Biorem has $2.15M in long term debt and an unused $3M credit facility, both at very good terms.

Cash Flow:

$2.3M of operational cash flow generated midway through the year, a $4.3M improvement from burning $2.1M at this stage last year. The company does have some pretty dramatic swings within their working capital adjustments so they are likely prone to some cash flow lumpiness from quarter to quarter, but this improvement over last year is pretty legit with a $1.8M improvement to last year prior to working capital adjustments.

They purchased $366k in assets and paid down $270k worth of debt YTD. Overall their cash position has improved by 70% in the last six months.

Share Capital:

The share cap presentation within these financials suck balls. Yeah, I said it

Very tight outstanding float with 15.7M shares outstanding with very small dilutive measures of 200k options exercised in the past 18 months

3.7M options outstanding (had to go back to their annuals again). All are in the money but expiry dates are between three and nine years

Biorem has a very conservative and retail friendly 5% SBC plan and the world would be a better place if more small cap stocks followed.

A miniscule 2% insider ownership number. 8,000 shares have been purchased on the the open market by insiders over THREE years. My kids allowances over three years are higher

Income Statement:

Barn burning top line with a 70% revenue increase over last years Q1 with $7.3M in revenue against $4.3M. YTD looks just as mouth watering with $13.2M, up 77% from $7.45M

Their gross profit rate isn’t sexy, but is improving with a 40 basis point improvement in Q2 to 22.7%, and a much more dramatic 1200 basis point improvement to 26% vs only 14.4% through six months last year.

What Biorem does extremely well is run a tight ship with operational expenses, and they have had excellent conversion on their sales growth this year with opex increasing by only 12% in the quarter, and 32% YTD, and that is on 70% and 77% more revenue growth respectively.

The strong growth, improved margins and conversion on expenses translates to a much improved bottom line. A $600k improvement in the quarter and a $1.8M turnaround YTD, in both cases going from a loss last year to profitability of $462k in net earnings in Q2 and $926k YTD.

Overall:

A very impressive first look at Biorem despite some issues with how they actually present their financials. I hope someone from the company reads this review and adds additional disclosure to their future quarterlies.

What about value? $31M TTM revenue puts it just a little over a 1.1 Sales to MC ratio and at an EV/EBITDA ratio of under seven, heck yes I’d say there is a little more meat on the bone here even with the share price appreciation so far this year.

I’m not a big backlog guy as I like more guarantees in life, but bookings in the quarter were $13M and they have a $57M backlog that they estimate most of that will be seen on the revenue line in the next eighteen months. That could result in a future TTM in the area of $40M.

Like anything, there are some risks here too. Revenue, margin and cash flow could be lumpy as well as long sales cycles due to the nature of their business. The tight float doesn’t offer a lot of liquidity and along with that comes with the potential of higher volatility. But with all that said, don’t be surprised if I slap the ask in the near future.

A rare initial four stars.

Buy Wolf a coffee which goes towards website maintenance costs

Have an request to review a stock you are interested in? Visit the TSA discord to make your request in our dedicated channel or email us at thewolf@wolfofoakville.com

Chat with me and 2900+ other members daily in the TSA Discord.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings and I do so without compensation. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.

Nice report. Surprised there wasn’t much movement after earnings.

What would you consider a realistic exit multiple for this business? It's a microcap, low quality, growth will most likely slow down. If the stock falls out of favor it would not surprise me if it trades around a 10 PE in a few years from now. In my base case I get to 0,25 CAD (diluted) EPS end of 2027. With a PE of 10 there would barely be any upside left from here on. Curious what your few is on this.