Omni-Lite Industries FINS Review

Q2 2024 (3.5 / 5) * Archive originally posted June 16, 2024

This one was recently put into my Twitter mentions. Typically, I cringe when someone does this as more often than not, it turns out to be a pile of dog shit. But I took a quick look and didn't hate what I saw, so decided to do a deeper dive here. The stock has been on a tear YTD more than doubling up to a close last Friday of $1.08 and market reacted quite positively to these financials. So is there any more juice left in the tank here?

Balance Sheet:

Strong start with a current ratio of 4.4 with deferred revenue removed and consists of $1.1M in cash, $2.8M of receivables, nearly $5M worth of inventory against only $2.05M worth of liabilities due over the next year. No long term debt but do have $5.56M tied up in long term leases. While their current ratio is strong, I wouldn't say the same for their liquidity with cash only making up 12% of current and under 5% of total assets. While they are not planning to take any A/R impairments the 45% of their receivables over 30 days is a little cause for concern, but the company also does not list their credit terms to know how much of an issue this might be. $5M of inventory is a very large amount to carry for a nanocap, and with revenues under $4.3M, inventory turnover is well under 4, but they were definitely much more productive and efficient this year over last.

Cash Flow:

Positive cash flow from operations of $260k in Q1, 24% better than Q1 a year ago, and if their is no concern about their receivables and they continue to be more productive with their inventory, I would expect this to trend much better as the year progresses as the company was negatively impacted by both in Q1 working capital adjustments. Before these adjustments, they nearly doubled their OCF. After lease costs and $150k in asset additions, they pretty much ended the quarter with the same amount of cash they began with.

Share Capital:

Tight float with just 15.4M shares outstanding

1M options outstanding, all of which ITM

1.4M warrants but just 200k currently ITM

Per YF, 11% insider ownership

One director with some aggressive open market buying in May

Income Statement:

Company ripped the doors off in Q1 with a 57% revenue increase to $4.29M, up from $2.73M in the comparable quarter. If you liked the revenue metric, you're gonna love the gross profit metric which more than doubled, going from 12.9% to 28.6%, so on 57% revenue growth, grew their gross profit dollars by 3.5x! The company operated extremely lean in the first quarter with SG&A costs only at 7.5% of revenue, so while the company doesn't produce sexy overall margins like you would see in other sectors, they can still put some serious dollars on the bottom line with a lean expense structure and that is exactly what they did with Operating Income of $801k, over a $1M turnaround, and Total net income of $415k, a $550k improvement.

The company is also firmly in bed with California Nanotechnologies ($CNO.V), owning about 16% of their shares. I also upgraded CNO in January in my latest review of them which you can read here. Due to the great performance of those shares they had a one time unrealized gain of $1.3M taking their total comprehensive income to $1.74M, over a $1.8M turnaround from Q1 of last year.

Overall:

Pretty outstanding performance out of the gate for these guys. I think the biggest question I have is the stock has been trading for longer than my kids have been alive, and the current CEO has been there for six years as has most of management, so why did the light-switch finally just get turned on?

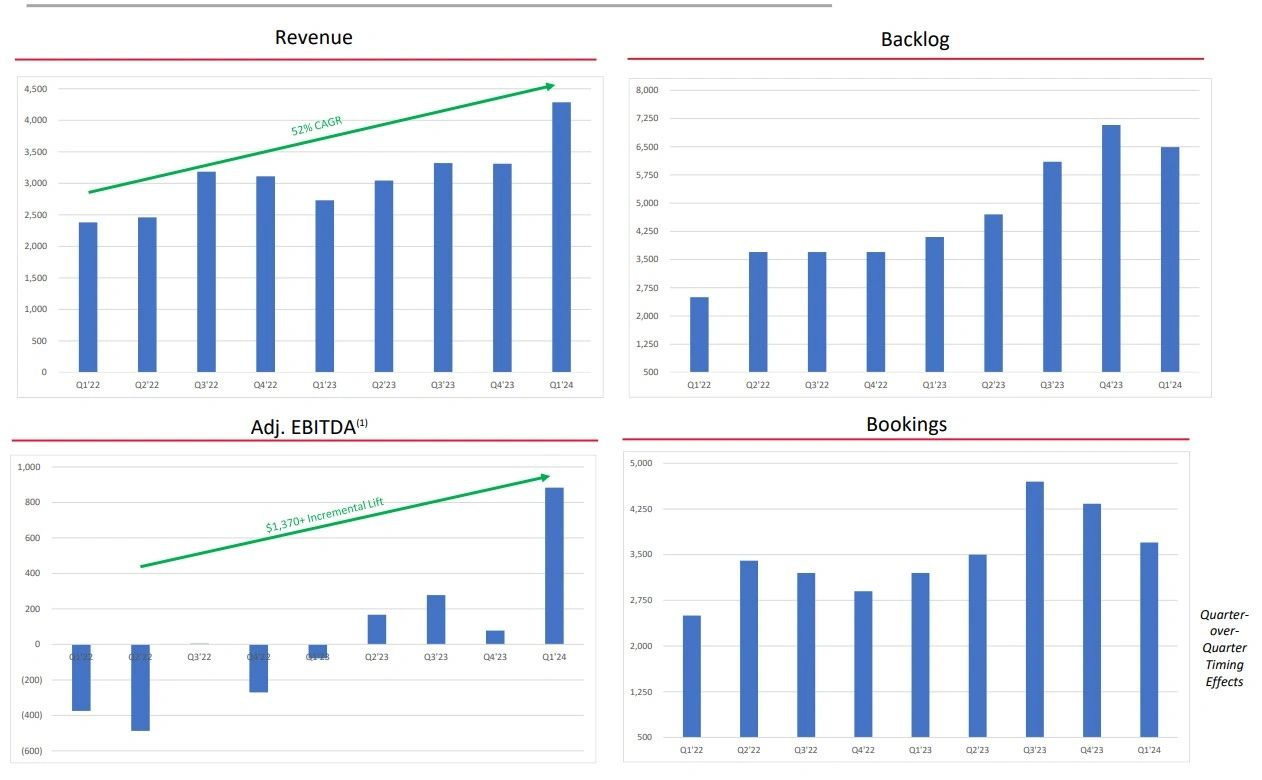

The investor deck contains additional bullishness showing their progressing, although slightly lumpy revenue growth and improving backlog. Most most impressively was their improved profitability which came from both margin improvements and getting extremely leaner within operating expenses.

Their outlook, while not timeline specific is bullish as well with additional 50% growth expected split between organic and inorganic, and gross margins of up to 50%. From the mid teens to 50% would be something.

With extrapolated revenues the company is trading at under 1 MC/Revenue ratio with an EV/EBITDA ratio of around 7, which I read into some value at this performance. If they can grow like they are saying they can in their investor deck with the margins shown, there could be plenty of value still here. Solid initial 3.5 stars and I want to know more about these guys.

Have a request to review a stock you are interested in?

Paid subscribers have priority access to request financial reviews of stocks they have interest in. Request via subscriber chat, DM or email at thewolf@wolfofoakville.com

Chat with me and 3000+ other members daily in the TSA Discord.

Disclaimer:

My intent is for my reviews to be a bolt on to due diligence that you have already completed. I receive dozens of review requests a week, therefore my own DD may be great or none whatsoever. Unless otherwise stated or implied, my opinions are on the financial performance of the company based on their most recent filings. I conduct these reviews to assist other retail investors whose research skills are limited when it comes to reviewing financial statements. I do not accept compensation of any kind from company’s I review.

Wolf FINS Reviews are intended to be informational and are based on personal opinion. They are not intended to be financial advice, and all readers are encouraged to perform their own due diligence prior to their investment decisions, including discussions with their investment advisor.